UPGRADING DONE

RIGHT WITH SUNNY

Are you keen to find out THE FOLLOWING regarding your home?

-

What can I upgrade to based on my situation safely?

-

Can I really own a private property stress-free?

-

What are the best projects for me to build my capital comforably?

Find out the answers to these and more during our free 1-Hour consultation!

There are 5 main options when the day comes to upgrade:

1. UPGRADING TO A SPACIOUS RESALE HDB

2. UPGRADING TO AN EXECUTIVE CONDO

3. UPGRADING TO A RESALE PRIVATE CONDO

4. UPGRADING TO A NEW LAUNCH CONDO

5. UPGRADING TO A LANDED PROPERTY

Are you doing your

HOME UPGRADING

the right way?

Over the years, I’ve asked my clients who want to upgrade their homes, whether it’s an HDB, Condo or Landed, the following question:

How do you ensure your upgrading leads to:

Strong capital appreciation of your home

Safely knowing your home will be an asset that appreciates continuously

Spare cash from the sale of your previous home

And NOT the following:

The answer is by knowing these

4 items:

Number 1

The 4 options of upgrading and the pros & cons.

Learn what are the pros and cons of each one of the options and how each of them will help you to maximize your profits.

Understand why if you’re looking to profit, why selecting a new launch can potentially yield better returns than a resale Condo/Executive Condo!

Number 2

The 4 options of upgrading and the pros & cons.

Learn what’s the actual value of your home and based on your current financial situation, we’ll plan:

1. Your financial roadmap to ensure you can retire safely

2. Ensure your financial security through the best property investments that are within your means.

Number 3

Selecting the best property to ensure you maximize your profits.

Learn how to select the right properties with our strategy, and how some of our clients have earned more than SGD$100,000 if they had selected the neighboring property!

Number 4

Current market situations & when is the best time for you to sell & buy.

We’ll guide you how to study market trends and cycles to decide when is the best time for you to sell & buy for Maximum profit.

CAN I UPGRADE SAFELY?

Get Your Latest Housing Report Here!

Are you looking to be like them and earn from their property?

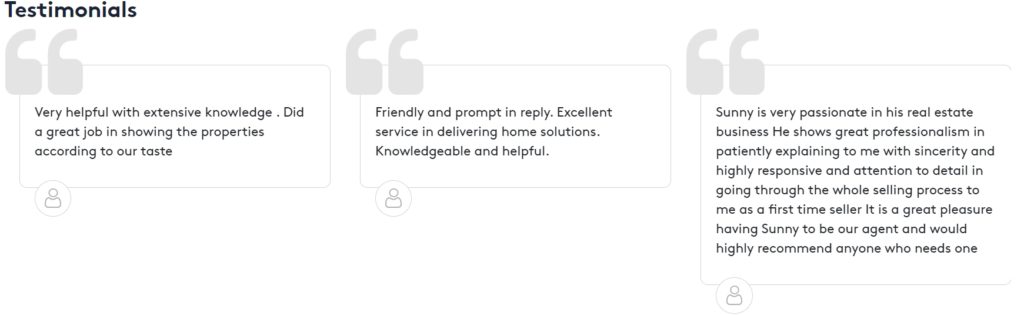

Sellers’ Success Story

Mr and Mrs Lee, both 35 years old, have a combined income of $8,000 came across our Facebook post and contacted us.

Original Plan:

- To sell their 4-room HDB flat and buy a resale Executive Maisonette.

After having a planning session with us:

- They upgraded to a 4-room Condominium STRESS-FREE and without touching any of their savings

- Keep a CASH reserve of ~ $150,000

With a clear asset progression road-map tailored and planned for them, they are even thinking of investing in a second property!

More Possibilities through tailored Asset Progression

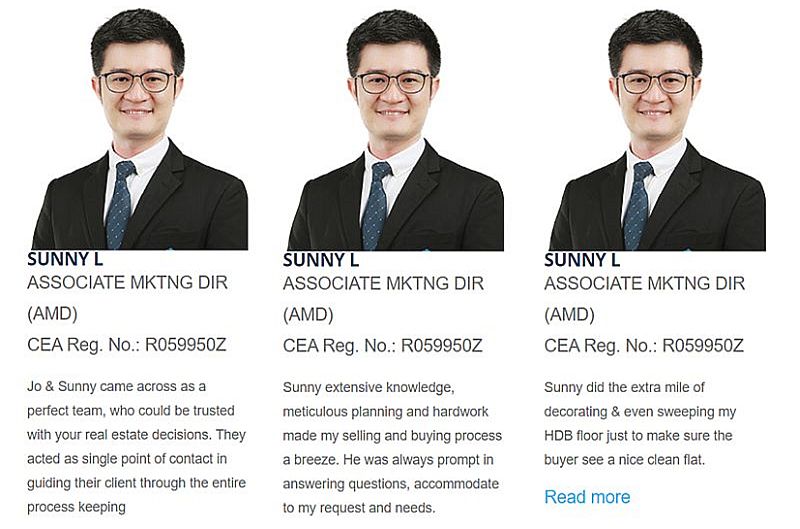

Let me be your

Advisor, Friend & Realtor

I’m Sunny, a realtor & investor with PropNex.

It is my commitment to provide guidance & assistance in real estate management and investment with integrity for my clients.

Coming from the Project Management background, I’ve developed a high level of structuring solutions within stipulated timeline and budget and I excel at managing risk.

I specialize in detailed financial analysis and using creative techniques to ensure home buyers find their dream home and homeowners to sell at the right price under the best terms.

Over the past few years, I’ve explained these questions and answers to my clients and many of them have done their upgrading the right way!

Every housing decision is an important one.

Let us make it the best for you.

Find out the answers to these and more during our free 1-Hour consultation!